•

Embedded financing has been around for decades and it started as a layaway program where shoppers will start paying for the goods and services in reverse. Meaning that they will pay to the merchants until the full price of the product and services are paid before they receive the product and services.

With today’s technology, payment rails and the insatiable demand to push more product and services, embedded financing or BNPL (Buy Now Pay Later) is taking over the world but sometimes the interest between lenders and merchants are misaligned putting consumers in a precarious financial situation.

What is embedded finance?

Embedded finance is a way to interject financing offers to purchase the product and services while the consumer is making a critical purchase decision.

Traditionally, the staff member will talk about financing options when their clients are making the purchase decision. It will sound something like “... would you like to use a credit card, cash or cheque?” and when all else fails, the staff member might hand over a few brochures to the customer and tell them to apply for financing with pure-play lenders.

The customers have no experience talking to lenders why they are deciding on an eyesight corrective surgery and this out of body experience of contemplating financing options is a big distraction and the merchant might lose the deal all together.

If the customer goes through with financing offline asynchronously, the lender will contact the merchants and reschedule a shopping experience for the customer to come back which makes the entire buying and selling process a drawn out process. Leaving the customer to seek out other means of purchasing at every turn.

Embedded finance in today’s internet age

To shorten that decision making process for both consumers and merchants, embedded financing has moved to an online, digital process. Sometimes the decisions are made instantaneously without the shopper leaving the store.

However, there are many unforeseen consequences that are just now dealing with and trying to understand the psychology of it all after a decade of in-store financing that’s carried out online and an approval decision is rendered in real time.

The embarrassment factor

Depending on the financing partner the merchant is working with, they either have a great deal of influence or nothing at all. Let’s break down the unavoidable embarrassment factor of in-store financing.

Most of the merchants today work with a pure-play lender, sometimes they are called a BNPL or Buy Now Pay Later lender. These lenders will work out a few fundamental agreements with the merchants. One of which is the approval rate and the other is the merchant discount rate.

What is the approval rate and what does that have to do with the embarrassment factor? The approval rate is how many applicants BNPL lenders are willing to approve for every 100 that walks through the doors. Sometimes these BNPL lenders have not had the chance to study the demographics of the consumer that walks through the merchant’s store front. Most of the time they are just using an average number to guess the approval rate based on their historical numbers that may or may not be applicable to the actual business they are financing.

Most of the time, the BNPL lenders will start conservatively if they don’t understand the business or getting into a sector that’s brand new to them. In reality, the approval rate might be much lower than what’s estimated.

When this happens, sometimes 50% of the clients get declined and the other 50% approved clients might not get approved for the amount of money they need to purchase the goods or services.

When the client applies in store while the store staff is waiting and gets a declined decision, the embarrassment of it all backfires immediately. It’s worse than getting a declined decision at home working with lenders (bouchoure guys) offline.

And when the client does get an approval but they didn’t get the approval amount they need to finance the purchase, it then becomes even more awkward. The client is being told that they are good but just not good enough and might have to shell out down payments to cover the shortfall.

Either way, when a merchant works with a lender that doesn’t understand their business, their clients or their product offerings, these one-size approval rate and approval amount simply doesn’t work.

Sometimes these relationships are called in-direct relationships where the lenders worry about one set of criteria to control for risk while the merchants struggle with moving more product and services.

How to fix this misalignment of interest?

Sometimes we see embedded finance done right. Most of the major car manufacturers have their own financing arm. For example, Toyota Motors has Toyota Financial Services. Why? Because they want to save the embarrassment of having their car buyers financing elsewhere that might get declined.

Also, their financing arm and their retail outlets are in lock step making arrangements to push more of their own cars on the street. Here are some of the reasons why building your own embedded financing stack is the only way to not get cooked with pure lenders with misaligned interests.

First, the approval process is tailored to the actual product and service the merchant is offering. Their in-house lender understands the type or product, cost and the demographics of their shoppers. They will tailor a lender solution for the purposes of selling cars. They understand the cost is much bigger than a usual consumer product and the duration of these loans are typically longer in years and not in months. They also understand the consumer is sensitive to interest they might have to pay over the period of the loan.

Most in-house financing solutions can work with their counterparts to adjust for the cost of funds such as interest and fees in order to move products and services en masse. In other words, both parties can share the pain to achieve a common goal.

We believe that the only way to have a successful lending program is to tailor the lending product to the product and services offered. The holistic approach is where you ultimately win and achieve the common goal of moving more product and services.

Introduction of risk based pricing in embedded finance

What is risk based pricing?

Risk based pricing is not a new concept but it’s hard to adopt because of lack of technology. Risk based pricing is the setting of the price of the interest rate, APR or fees based on a variety of factors including all aspects of the borrower's creditworthiness and the ability for merchants to deliver their promised product and services without complaints.

For instance, one of the major factors in financing in the embedded finance industry is what’s called a “Merchant Discount Rate”. A merchant discount rate is essentially a discount merchants give to lenders in order to shift the financing cost of the consumer to the merchants themselves to make it easier for their clients to finance the product or services.

Here’s an example, if the merchant doesn’t give up any discounts, the lender might have to shift the interest rate completely to the consumer. Instead of a 0% interest rate financing product which is fairly popular with BNPL lenders, they might have to charge the consumer 29.99% APR to borrow what’s needed to purchase the product and service. This sounds expensive and illegal in some countries.

To make this interest bearable or making it completely disappear, the merchant will bear the burden and give the lender, say 20% discount on the MSRP to alleviate the consumer to have to pay the 29.99% interest to cover potential losses to the lenders.

This merchant discount rate can be adjusted and should be adjusted based on the riskiness or creditworthiness of the consumer. If someone is applying for financing with a great credit history, the merchant discount rate will be a lot less, or even 0 and perhaps the consumers will be okay getting charged a 4.99% interest rate as a reward for their credit history.

Conversely if the borrowers have less than stellar credit history and the merchant still would like to offer their product and services, they might still offer financing but perhaps put up more merchant discounts (eating into their profit) and work with their inside financing arm to get the deal done.

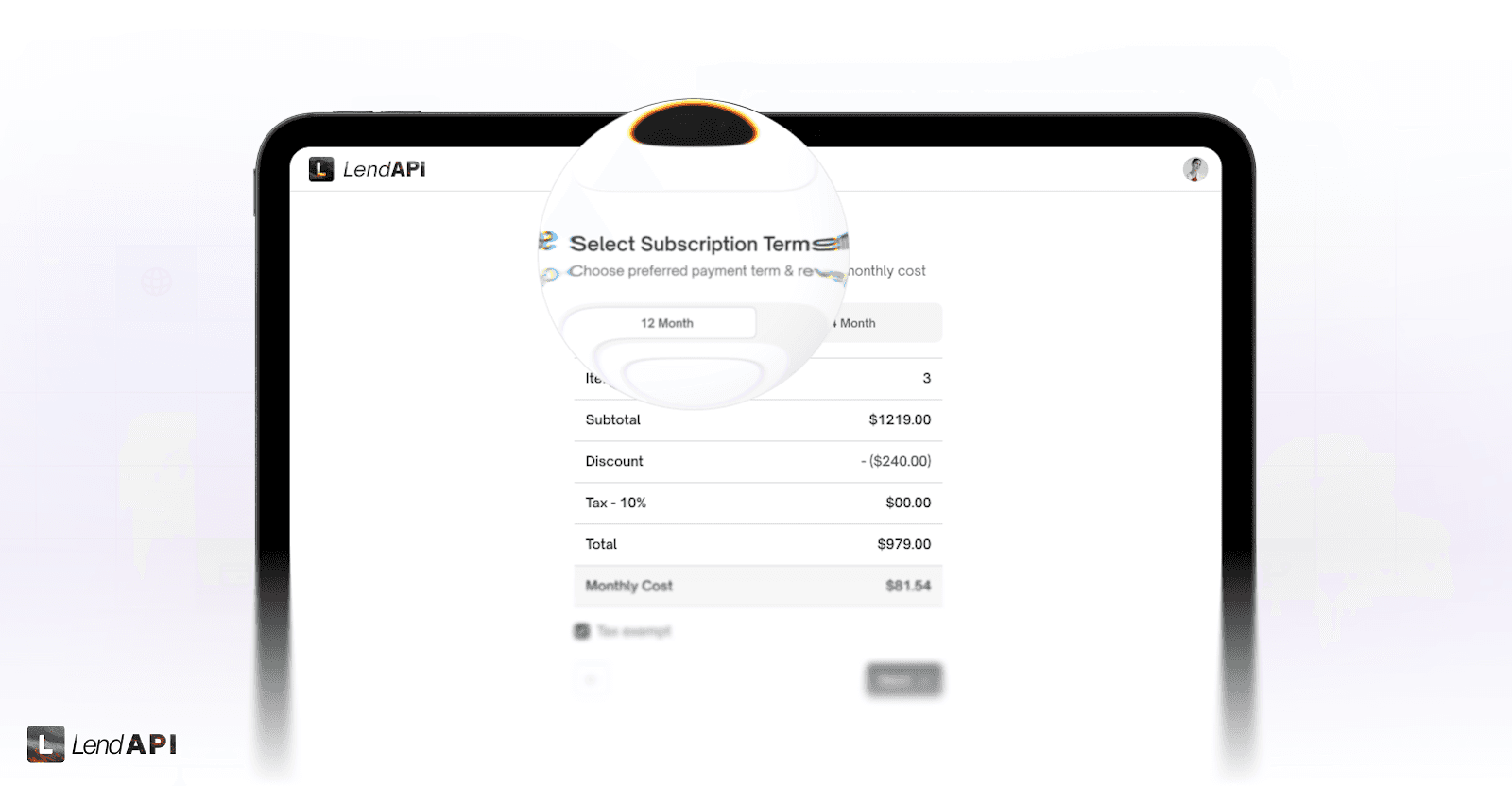

When risk based pricing is implemented correctly where the merchant and their financing partners work hand in hand to adjust for risk with merchant discount rates, down payments from the consumer as well as the interests and fees collected to hedge risk, a successful embedded finance product will have a better chance of success.

The embedded financing technology stack

The embedded financing technology should blend the shopping experience and risk management technology together.

It all starts with a shopping experience where the merchant is scanning or entering product and services information into an interface. Whether the technology stack is pulling information from supply chain systems or inventory catalogs, the embedded financing technology stack should be aware of all of the product and services the merchant is offering.

The decisioning technology should have risk based functionalities built in so the appropriate offer is generated based on the applicant’s credit worthiness, the margin on the product and services offered and the willingness for the merchant to take on additional risks such as whether the client is a new client or a repeating customer.

The technology stack should also contemplate other factors from external sources as well. For example, credit bureaus in various countries to examine the credit worthiness of the consumer. If Open Banking is prevalent in your country, a customer’s bank account and their personal cash flow is another great indicator of their ability to repay the loan.

Even in an in-store experience, the merchant might want to perform an identity verification process to verify the shopper’s identity and make sure that the credit bureau report is reporting on the person standing in front of you.

The shoppers history with the merchant is another data point a sound embedded financing program should have. In some situations, the service consumer purchased is delivered over time during the repayment period. This makes the credit decision slightly easier, if the client stops paying the remainder of the service rendered might be paused before the client and the financing department work out any potential issues and get back on track.

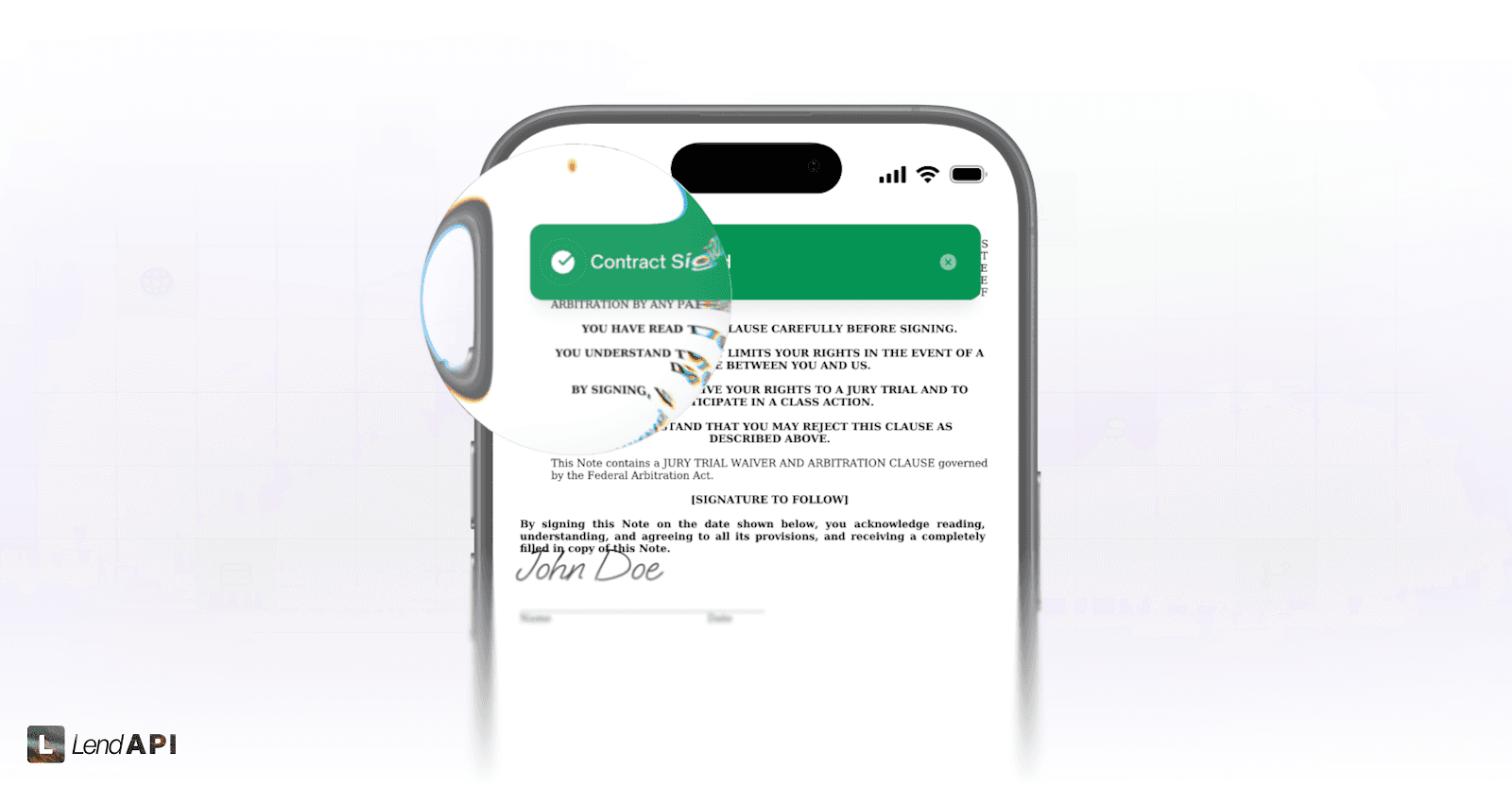

The tech layer in embedded financing also needs to have a deep understanding of compliance. From calculating interest rates and payment amounts to consents and signing of promissory notes, the system needs to know how to hand off the experience from the merchant to the borrower to gather the borrower's consent and their signature on purchase contracts and promissory notes.

Embedded finance is a $500 billion dollar market world wide

Embedded finance is a $500b market world wide and although there’s been a lot of innovation seen in this space for the past 10 years, we believe that giving merchants more control with customized lending experience that has everyone’s interest aligned including the merchants, shoppers and lenders will be an even bigger win for everyone involved.

The US, Canada and Mexico represent $140 Billion dollar market size and we are just in the first inning of developing custom, private labeled embedded financing platforms for small to large merchants in the Americas.